Chart of Accounts (AGPR): A Complete Information for Public Sector Entities

Associated Articles: Chart of Accounts (AGPR): A Complete Information for Public Sector Entities

Introduction

On this auspicious event, we’re delighted to delve into the intriguing matter associated to Chart of Accounts (AGPR): A Complete Information for Public Sector Entities. Let’s weave attention-grabbing data and supply recent views to the readers.

Desk of Content material

Chart of Accounts (AGPR): A Complete Information for Public Sector Entities

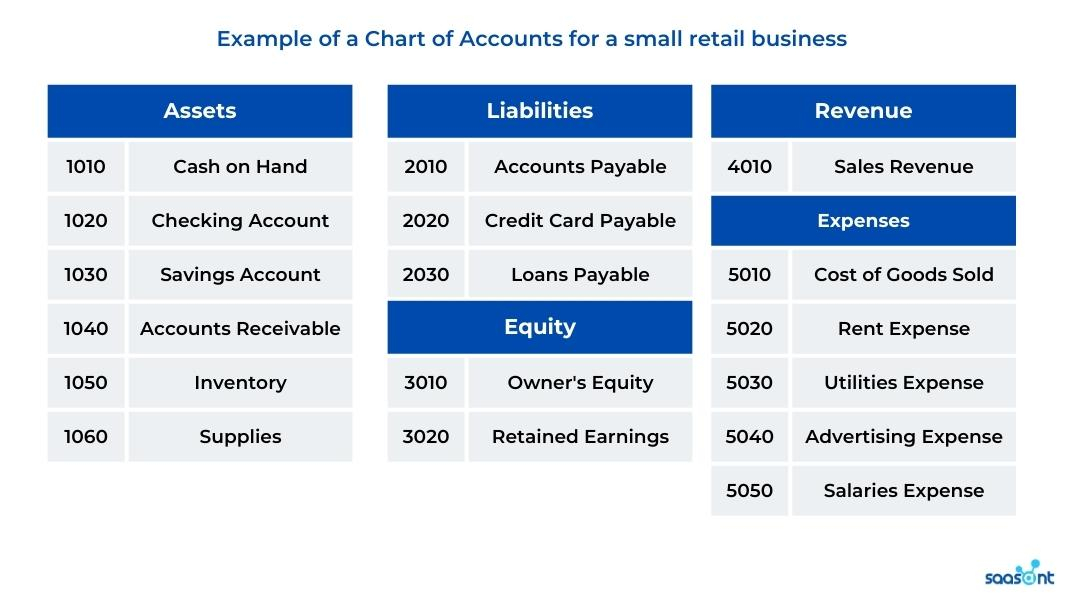

:max_bytes(150000):strip_icc()/chart-accounts-4117638b1b6246d7847ca4f2030d4ee8.jpg)

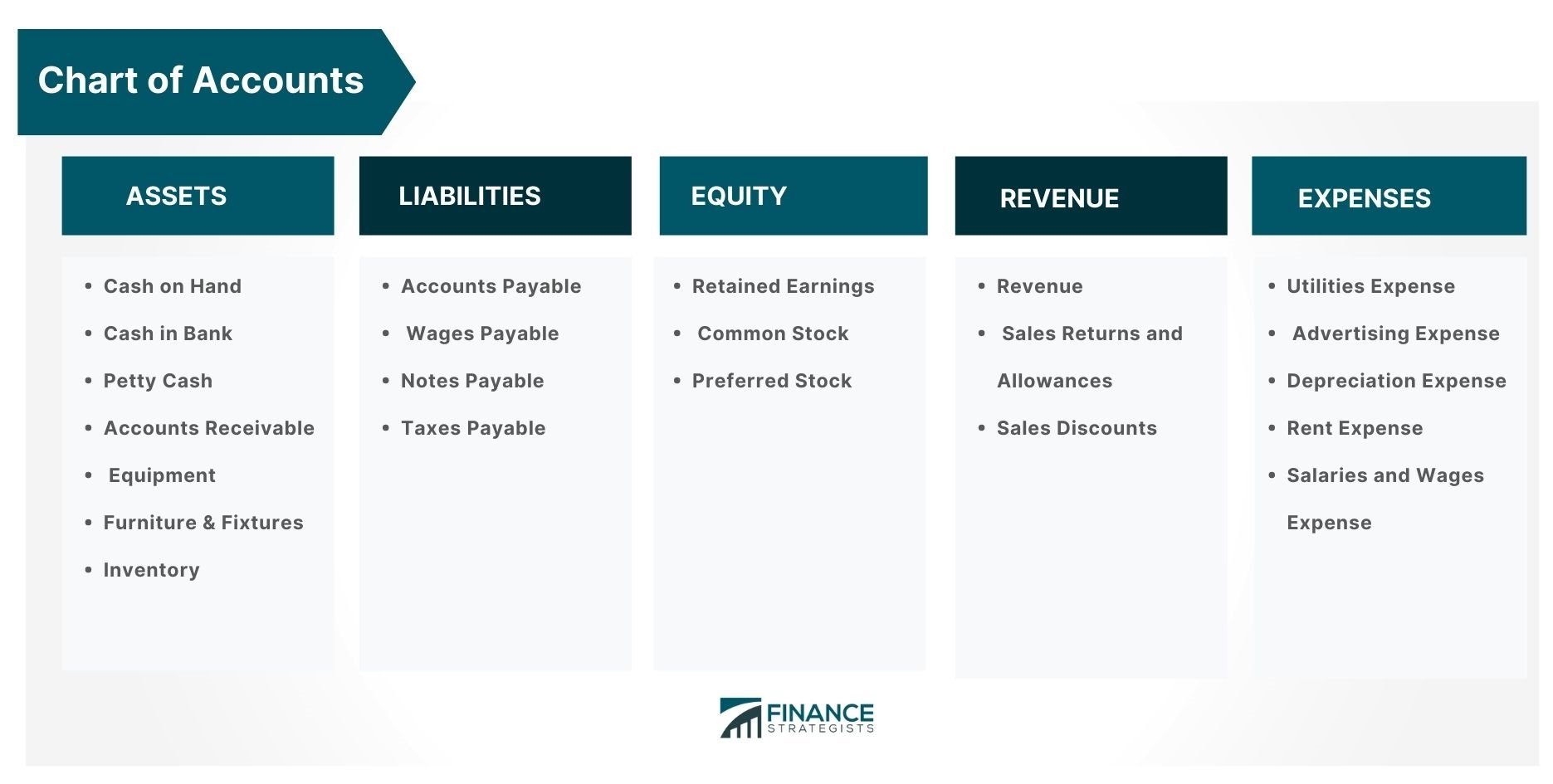

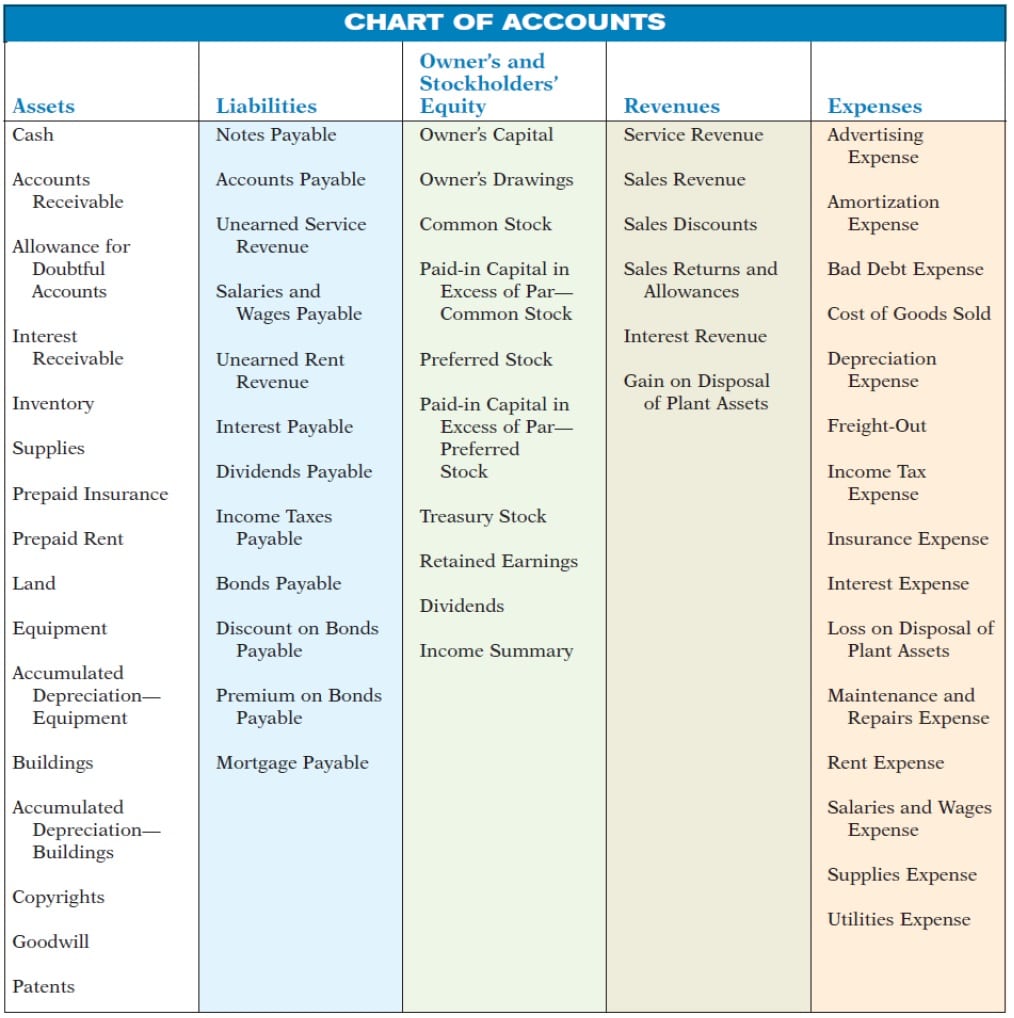

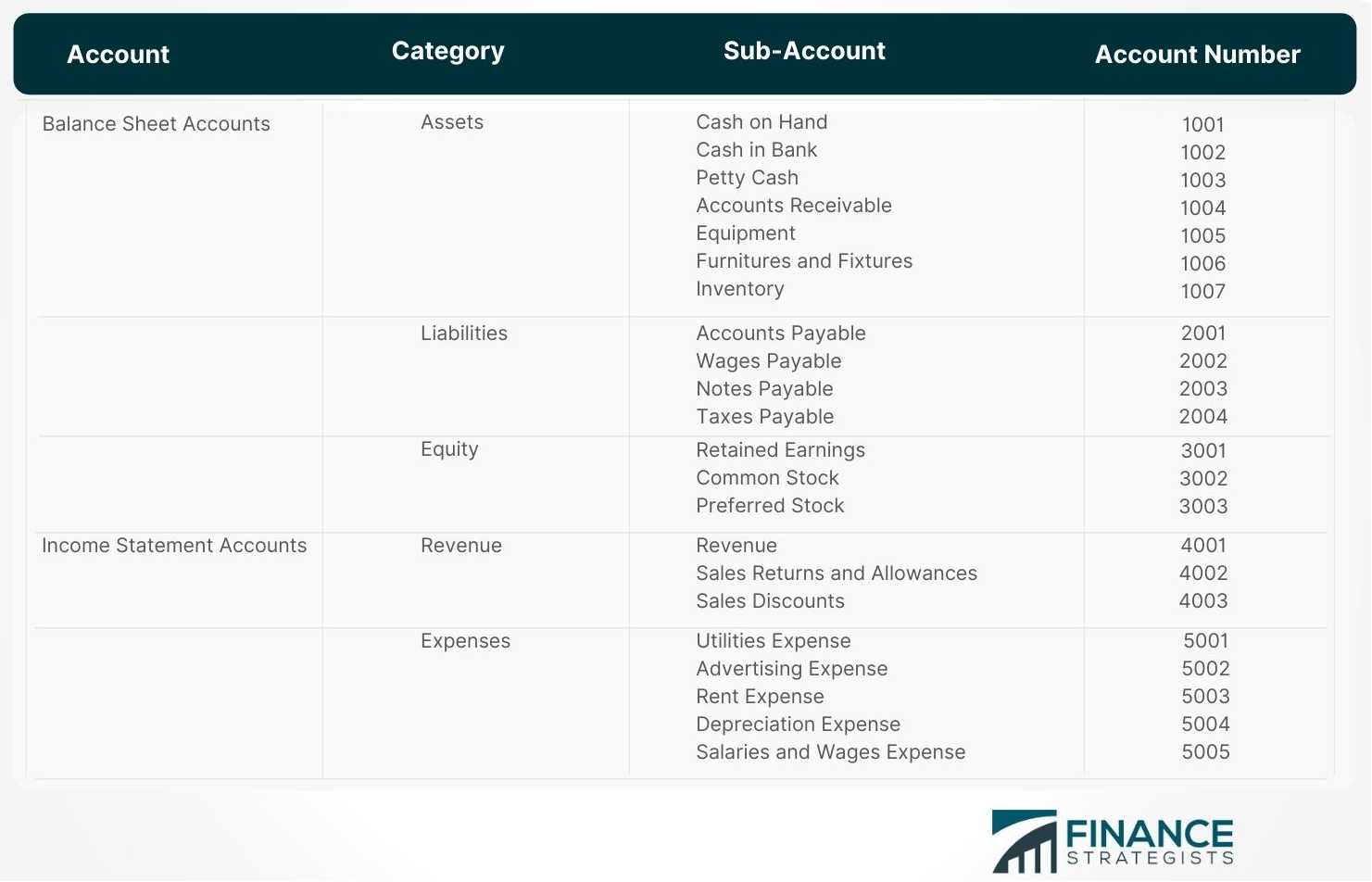

The Chart of Accounts (COA) is the spine of any group’s monetary reporting system. For public sector entities working underneath the ideas of Typically Accepted Public Sector Accounting Ideas (AGPR), the COA holds even larger significance, guaranteeing transparency, accountability, and compliance with laws. This text delves into the intricacies of the AGPR Chart of Accounts, exploring its construction, key components, advantages, and challenges in implementation and upkeep.

Understanding the AGPR Framework:

AGPR, or Typically Accepted Public Sector Accounting Ideas, offers a standardized framework for monetary reporting within the public sector. Not like non-public sector accounting requirements like Typically Accepted Accounting Ideas (GAAP), AGPR emphasizes accountability to the general public and adherence to legislative mandates. A well-structured COA is essential for reaching these objectives. The COA serves as a structured listing of all accounts used to document monetary transactions inside a public sector entity. It ensures consistency in recording and reporting, making it simpler to trace revenues, expenditures, property, and liabilities.

Construction and Key Components of an AGPR Chart of Accounts:

A typical AGPR COA is hierarchical, typically using a multi-digit numbering system to categorize accounts based mostly on their nature. The construction varies relying on the particular wants and dimension of the entity, however frequent components embrace:

-

Fund Accounting: AGPR typically necessitates the usage of fund accounting, separating monetary sources into distinct funds based mostly on their goal (e.g., Basic Fund, Particular Income Fund, Capital Tasks Fund, Debt Service Fund, Enterprise Fund, Inside Service Fund, Belief and Company Funds). The COA displays this separation, with every fund having its personal set of accounts. This ensures that sources allotted for particular functions usually are not misappropriated.

-

Object Codes: These codes classify expenditures by their nature (e.g., salaries, hire, utilities, provides). This granular stage of element permits for detailed evaluation of spending patterns and facilitates price range management.

-

Program Codes: These codes hyperlink expenditures to particular authorities packages or initiatives. This enables for efficiency measurement and accountability for the usage of public funds.

-

Exercise Codes: These codes additional refine the classification of expenditures by figuring out particular actions inside a program.

-

Location Codes: These codes determine the bodily location the place expenditures occurred.

-

Account Sorts: The COA consists of accounts for varied asset, legal responsibility, fairness, income, and expense classes, according to double-entry bookkeeping ideas. This ensures a balanced accounting equation always.

-

Management Accounts: These accounts summarize the balances of subsidiary accounts inside a selected fund or class. They supply a high-level overview of monetary place.

-

Chart of Accounts Handbook: A complete guide accompanies the COA, offering detailed definitions and tips for utilizing every account. That is essential for consistency and accuracy in monetary recording.

Advantages of a Properly-Designed AGPR Chart of Accounts:

A correctly structured and maintained AGPR COA affords quite a few advantages:

-

Improved Monetary Reporting: The COA facilitates the preparation of correct and well timed monetary statements, complying with AGPR and different related laws.

-

Enhanced Transparency and Accountability: The detailed classification of transactions enhances transparency, permitting stakeholders to simply perceive how public funds are getting used.

-

Higher Funds Management and Administration: The detailed categorization of expenditures permits efficient price range monitoring and management, stopping overspending and selling environment friendly useful resource allocation.

-

Improved Inside Controls: A well-designed COA strengthens inner controls by offering a framework for segregation of duties and authorization procedures.

-

Facilitated Auditing: A standardized COA simplifies the audit course of, making it simpler for exterior auditors to confirm the accuracy and reliability of monetary data.

-

Information Evaluation and Resolution-Making: The structured knowledge supplied by the COA permits insightful evaluation, supporting knowledgeable decision-making by authorities officers.

-

Streamlined Processes: A well-designed COA can streamline monetary processes, lowering guide effort and enhancing effectivity.

Challenges in Implementing and Sustaining an AGPR Chart of Accounts:

Regardless of the quite a few advantages, implementing and sustaining an AGPR COA presents a number of challenges:

-

Complexity: The hierarchical nature and detailed classification necessities could make the COA advanced to design and implement.

-

Customization: The perfect COA must be tailor-made to the particular wants of the entity, which is usually a time-consuming and resource-intensive course of.

-

Information Migration: Migrating present monetary knowledge to a brand new or revised COA is usually a vital enterprise, requiring cautious planning and execution.

-

Coaching and Consumer Adoption: Satisfactory coaching is essential to make sure that all customers perceive and appropriately apply the COA. Resistance to alter can hinder adoption.

-

Upkeep and Updates: The COA must be repeatedly reviewed and up to date to mirror adjustments in laws, accounting requirements, and organizational construction.

-

Integration with different Techniques: The COA must be built-in with different monetary and administration data methods to make sure seamless knowledge move.

-

Price: The preliminary growth and ongoing upkeep of a COA may be costly.

Future Traits in AGPR Chart of Accounts:

The evolution of know-how and accounting practices is impacting the AGPR COA. Future tendencies embrace:

-

Elevated Use of Know-how: Automated methods and knowledge analytics are more and more getting used to handle and analyze knowledge from the COA.

-

Information Standardization: Efforts are underway to standardize COA buildings throughout totally different public sector entities to enhance knowledge comparability and reporting.

-

Integration with Efficiency Administration Techniques: The COA is more and more being built-in with efficiency administration methods to hyperlink monetary knowledge with program outcomes.

-

Cloud-Based mostly Options: Cloud-based accounting methods have gotten extra prevalent, providing larger flexibility and scalability for managing the COA.

Conclusion:

The AGPR Chart of Accounts is an important instrument for public sector entities, guaranteeing monetary transparency, accountability, and compliance. Whereas implementing and sustaining a strong COA presents challenges, the advantages considerably outweigh the prices. By fastidiously designing, implementing, and sustaining their COA, public sector entities can considerably enhance their monetary administration and reporting, in the end serving the general public curiosity extra successfully. Steady enchancment and adaptation to evolving technological and regulatory landscapes are essential for maximizing the worth of the AGPR COA within the years to return.

:max_bytes(150000):strip_icc()/chart-of-accounts-984cd9454c364932b0cba045f56a6bb1.jpg)

Closure

Thus, we hope this text has supplied precious insights into Chart of Accounts (AGPR): A Complete Information for Public Sector Entities. We hope you discover this text informative and useful. See you in our subsequent article!